Table of content:

Image Source: https://www.swiftsalary.com/50-30-20-rule/

Financial trouble can affect anybody, regardless of income. We are dependent on a thriving economy and a stable income, after all. How do you make sure you’re financially prepared for the future?

Only about a third of Americans maintain a budget for their household. That means 70% of Americans are unprepared for financial strife. What about you?

Step 1: Determine Why You Need A Budget

You must first understand why you need a budget. It is especially crucial if you are budgeting for multiple people. Understanding why you need to manage your money will help you stick to your final plan better.

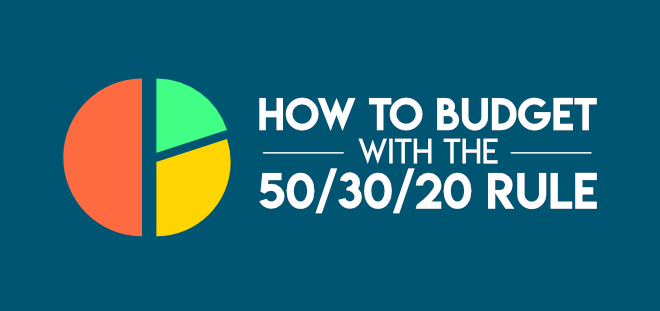

We’re going to discuss the 50/30/20 rule. According to this budgeting rule, 50% of your income should be going to needs.

30% of your income should be going to wants. 20% goes to savings and debt. Are you perhaps spending 45% on wants and 5% on savings?

It’s been shown that you are most likely to budget if you make at least $75,000 a year. Is your spending getting out of control?

Think about your financial fears. Then think about the solutions to those fears.

A budget is simply a spending plan meant to alleviate the financial burden. Once you have the reason behind your budget, you also have a goal for it.

Step 2: Determine Your Income After Deductions

Image Source: https://pittsburgh.cbslocal.com/2014/04/09/7-deductions-that-lower-your-taxable-income/

We have all calculated our income before getting our pay-stub and made the mistake of not deducting taxes. Don’t do that when you’re budgeting. Know the income tax rate where you live and know how to deduct it.

There are plenty of websites that can help you determine an approximate paycheck amount after taxes. The only problem is that there isn’t a way to know if they’re completely accurate. The best way to be accurate is to know your stuff and do the math yourself.

Also, don’t forget to include any income from side jobs you may have.

If you have deductions for a 401k from your paycheck, include that when tracking savings for retirement later. These are a part of that 20% from the 50/30/20 rule.

Step 3: Track Your Spending

Planning your spending means moving your money around; that requires knowing where it is in the first place.

Make sure you have your wants and needs in the right place. You should not be buying Starbucks using that chunk of income set aside for needs. If you run out of that 30%, then you’re done for the month.

Being diligent is one of the most important parts of the 50/30/20 rule.

Look at what income went toward necessities, what went toward wants, and what went toward savings and debt.

What percentage of your income goes to necessities? To wants and debt?

In 2016 the average American household earned $74,664. Out of that, expenditures averaged about $57,311. About 33% of their budget went to housing, while 17% went to transportation, and 5% went to entertainment.

How does your spending compare to these numbers?

Step 4: Adjust And Plan Your Spending- More About The 50/30/20 Budgeting Plan

Image Source: https://www.pennypolly.com/smart-money/how-much-should-you-save-each-month

Senator Elizabeth Warren popularized the 50/30/20 budgeting rule. She wrote about it in her book, All Your Worth: The Ultimate Lifetime Money Plan. The rule looks like this:

- 50% of your income goes to needs

- 30% of your income goes to wants

- 20% of your income goes to savings and debt management

Your needs are bills that must be paid. These include house payments, utility bills, and a minimum credit card or loan payments.

Cable and fabric softener might end up falling off your spending list; these aren’t necessities but wants. You have to narrow down what is worth spending money on. Is that enamel pin, custom made for your politician brother, worth it?

Also remember that with budgeting plans, the simpler, the better. Too many spending categories can over-complicate things. It’s fine to use only the 3 categories for needs, wants, and savings.

Step 5: Automate Your Bills

If you can automate any of your bills, you should. It will force you to make sure you have the money in the account beforehand. The bill gets paid no matter what, and you don’t risk an overdraft or a late fee.

Automating your necessary bills assures you that your needs are taken care of every month. This way you don’t end up spending your %50 on unnecessary things.

The 50/30/20 rule is prioritizing necessities. If something happens and you need the extra money, it’s okay to go without cable for a month. It’s not okay to go without water.

Automating your payments makes things easier and allows you to be more reliable. However, you should still check on these auto-payments every month. Automated systems do make mistakes, and you don’t want to pay late fees because of errors.

Step 6: Automate Your Savings

Image Source: Seven ways to automate your savings (alliantcreditunion.org)

A 2018 survey revealed that only 39% of Americans could cover a $1000 emergency. 44% wouldn’t be able to cover a $400 emergency that required out-of-pocket payment. The best goal to have is to have at least 3 months of emergency savings built up.

It’s best to automate your savings so that you aren’t tempted to skip setting them aside. In fact, the 50/30/20 rule exists so that you know exactly how much to save.

It’s easy to think about what you want to buy with your savings later. However, your savings on something you want isn’t what this part of your budget is for.

If you want to save up for a new cell phone, set aside money from your “Wants” category. This savings fund is meant to be a cushion in case anything happens. You only have 20% on savings and debt, so don’t spend it carelessly.

Step 7: Think Of The Future

Look at the big picture. One day you’re going to be old and dependent. It happens to all of us.

What then? Are you going to live off your kids and their money? Or are you going to have a retirement fund that takes you cruising with your spouse every year?

Do you have small children? Are they going to want to go to college?

Are you and your partner planning to have kids in the future? Should you start saving for a house and a baby now?

The 50/30/20 rule is meant to benefit your whole family. It’s an easy guide that assists you in planning far into your financial future.

Budgeting is about thinking and planning ahead. The best way to do that is to discuss your plans with your household. If you’re alone on your budgeting journey, take your time to figure out what you’re going to do.

Step 8: Keep Track of Your Progress on Savings And Debt

Image Source: https://www.makeuseof.com/tag/visualize-debt-stay-motivated/

There are plenty of ways to keep track of budgeting progress. Doing this also requires you to keep track of spending, which can sound a little overwhelming.

The 50/30/20 rule is also a great tool for when you’re feeling up to your eyeballs in numbers.

If you’re a manual individual and enjoy doing the work and organizing yourself, make a spreadsheet.

If you can’t be bothered, here’s a list of apps that can do it for you:

- Mint

- YNAB

- PocketGuard

- Goodbudget

- Personal Capital

- Clarity Money

- EveryDollar

Either way, remember to use just three categories for separating expenses. The 50/30/20 rule does it for you: needs, wants, saving/debt. Don’t create a list of a dozen categories for groceries, gas, utilities, cable, etc.

Remember that less is more. Money management is hard, so don’t make it more complicated for yourself.

Step 9: Be Resolved to Live with Your Budgeting

We said it once already: the 50/30/20 rule is about diligence. It doesn’t work if you aren’t going to stick to your categories correctly. The point of this rule is to help you manage to get you do the following:

- pay your bills,

- pay off your debt,

- create a savings cushion,

- manage to spoil yourself once in a while.

All of these steps up until now are there to lead you to this point: sticking with it.

Be determined to live with your budget.

Living with your budget can be hard. It requires learning some new habits:

- You may have to tell yourself “no” more often.

- You may have to operate on a cash-only basis. Leaving the debit card at home can force you into not spending extra money.

- You may have to go without luxuries – stop eating out or unsubscribe to Netflix.

Step 10: Review Your Budget And Regularly Spending To Make Sure You’re Staying On The Right Track

Image Source: https://sygnvs.com/budget-checkup-critical-components-nonprofits/

A budget should be an approximate estimation of what you’re going to spend. However, you can’t see the future, so it’s good to be flexible with monthly financial changes.

Some bills get paid only once or twice a year, like a bi-annual insurance premium. You may also pay off a credit card and end up with more spendable income.

Your 50/30/20 budget should be a tool that you revisit monthly or even every time you get paid. It is a means by which you are reaching your financial goals. It is there to make your life easier, so try not to see it as a chore.

Checking the budget helps you make sure you’re meeting your goals. If you aren’t, revise and adjust! The 50/30/20 is meant to be easy to follow, plan for, and revise.

Other Budgeting Methods

We discuss the 50/30/20 budgeting method in this article, but there are plenty of different ways. This method may not work for everyone. If you’re looking for other budgeting strategies, here are some alternatives and how they compare to 50/30/20 budgeting.

Zero-Sum Budgeting

It is one of the most detailed ways to budget. It basically involves keeping a real-time bank balance book that you consolidate your expenses with your income/budget. The goal is to come out at the end of the month with a difference of zero.

This method is for the more Type A budget planner, and probably someone who likes numbers.

How does it compare to the 50/30/20 method? There are a lot of numbers and math in zero-sum budgeting.

Pay-Yourself-First Budgeting

Image Source: The "Pay Yourself First" Approach to Budgeting | Budgeting, Pay yourself first, Personal finance blogs (pinterest.com)

This method is also called the “Leftover” method.

This system is for you if you don’t want a complicated budgeting method. Pay what you need for bills and set aside money for savings. After that, spend the rest of your money on yourself however you like.

This method is for people who have clear savings goals and don’t need a strict budget. It differs from 50/30/20 budgeting which prioritizes necessities. 50/30/20 is more for those who are experience financial hardship.

Envelope Budgeting

This method is cash-only and is a version of the zero-sum method. Write your spending categories on envelopes, then withdraw your income as cash. Spend out of your envelopes – if you overspend, you have to take money out of another envelope.

For instance, if you go grocery shopping, you will take your grocery envelope. At the register, you will pay out of that envelope. If you’re five dollars over your grocery budget, you have to reach into your “Gas” envelope.

Now you have five dollars less to spend on gas for your car. Unless you steal from another envelope. But you probably shouldn’t get in the habit of doing that.

50/30/20 budgeting is for people who like to plan. Envelope is for someone who tends to have spending issues.

Penny Tracking Budgeting

This method is a kind of real-time budget tracking that takes a lot of perseverance. For anyone with spending problems, it can be extremely eye-opening. Set your budget and then keep track of every cent you spend to make sure you’re following it.

You can actually penny track and use the 50/30/20 method at the same time. This is for you if you tend to have a hard time sticking to your percentage goals.

Conclusion

As of 2017, about 62% of Americans were in credit card debt, and 17.5% had student loan debt. What about you? Are you struggling because of a debt balance or a lack of savings?

Maybe your income is too low for your spending habits? Maybe you eat out too much, or you’ve into a rough spot with last-minute financial emergencies? If any of these are the case, you may benefit from the 50/30/20 budgeting method.

Have you budgeted before or are planning to? Were these 10 steps helpful? Are you going to try the 50/30/20 rule?

Are there some suggestions you’d like to share with other readers? Leave us a comment below and let us know!

Article written by

Ryan JohnsonAwesome! Share To :

Receive our news

5 Most Important Features to Look for When Buying Running Hats

Top Websites To Find Enamel Pins Designer